Sandwich Panel Manufacturing Market Size and Outlook 2032

Market Overview: Sandwich Panel Manufacturing 2023/2032

The global sandwich panel manufacturing market is forecast to double in less than a decade, reaching USD 20.51 billion by 2032 from USD 9.91 billion in 2023, with a Compound Annual Growth Rate (CAGR) of 8.4%. This growth is powered by rising demand for energy-efficient buildings, modular construction and the rapid expansion of cold chain infrastructure worldwide.

As a manufacturer of advanced sandwich panel production lines, Fineagles Advance Engineering closely tracks these market shifts to help partners scale with confidence. With continuous PU/PIR and mineral wool production lines designed for high-volume, export-ready production, Fineagles equips producers to meet both today’s demand and tomorrow’s sustainability and safety standards.

This article explores the forces shaping the industry of sandwich panel manufacturing from key materials and material trends to regional dynamics, challenges, and future outlook, giving you a clear view of where sandwich panel manufacturing is heading.

Table of Contents

- Market Overview: Sandwich Panel Manufacturing 2023 / 2032

- What Is Driving the Growth in Sandwich Panel Manufacturing?

- Applications Driving Sandwich Panel Demand

- Industrial and Commercial Buildings on the Rise

- Material Trends in Sandwich Panel Manufacturing

- Regional Breakdown of the Manufacturing Market

- Challenges Facing the Sandwich Panel Manufacturing Industry

- Future Outlook for Sandwich Panel Manufacturing

- Sandwich Panel Manufacturing on the Rise

- Frequently Asked Questions

- Get Ahead in the Market

What Is Driving the Growth in Sandwich Panel Manufacturing?

The rise of sandwich panel manufacturing isn’t just about replacing traditional building methods, it’s more about redefining them. Three major forces are accelerating this shift:

- Rapid Construction Needs: Urbanisation and industrial expansion in Asia, Africa, and Latin America demand faster, more cost-efficient building solutions. Prefabricated sandwich panels reduce build times by up to 40% compared to traditional methods.

- Energy-Efficient Building Regulations: Climate policies such as the EU’s Energy Performance of Buildings Directive and new U.S. and Indian standards are pushing for better insulation in every sector. Sandwich panels with low thermal conductivity meet these requirements.

- Expansion of Cold Chain Infrastructure: The global cold chain market is expanding rapidly, projected to nearly quintuple from about USD 316 billion in 2024 to USD 1.6 trillion by 2033, reflecting a 20.1% CAGR.

Together, these drivers make sandwich panels not just an alternative, but the preferred solution for modern, sustainable, and high-performance construction.

Applications Driving Sandwich Panel Demand

Online grocery shopping, and pharmaceutical distribution depend on temperature-controlled environments; cold storage and logistics infrastructure are expanding fast because of this. This is one of the biggest drivers of sandwich panel production growth.

Panels with polyurethane (PU) or polystyrene (EPS/XPS) cores provide strong insulation and resist moisture, making them ideal for refrigerated facilities. As countries like India and the U.S. expand rural cold chains to reduce food waste, demand for these panels keeps growing. To meet this need, Fineagles offers advanced PU and EPS sandwich panel production lines, helping manufacturers boost capacity and maintain consistent quality standards.

Industrial and Commercial Buildings on the Rise

Because of federal and private investments in warehouse and distribution center development, the U.S. sandwich panel market alone is expected to hit USD 3.35 billion by 2032.

Thousands of square meters of insulated metal panels are needed, because new industrial parks are being built rapidly in fast-growing economies like Vietnam, Indonesia, and Mexico. Factories, data centers, and commercial complexes are increasingly using sandwich panels for roofing and wall cladding.

Since sandwich panels are lightweight, they reduce structural load. Their durability also ensures long-term performance in tough environments.

Material Trends in Sandwich Panel Manufacturing

PU & PIR Sandwich Panels: Polyurethane Dominates by Type

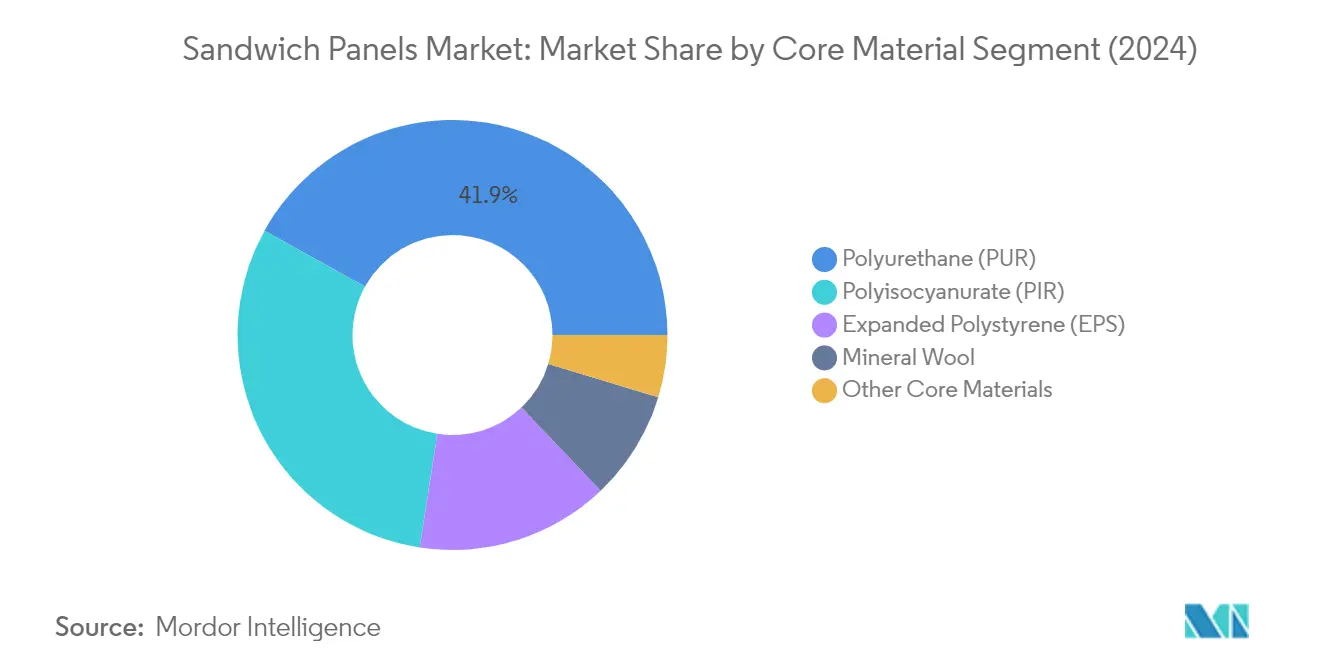

Sandwich panel market share by core material (2024). Source: Mordor Intelligence.

In 2023, the polyurethane (PU) segment held the largest share of the sandwich panel manufacturing market. This is because it offers:

- Superior thermal insulation

- Lightweight and strong

- Corrosion and moisture resistance

- Cost-effective for large-scale use

However, fire safety remains a concern. Because untreated PU cores can catch fire, stricter regulations have been introduced in some regions.

Fineagles addresses this with advanced PU/PIR production lines that help manufacturers produce panels meeting the latest safety and energy standards.

Mineral Wool Sandwich Panels Gaining Traction for Fire Safety

Mineral wool is gaining traction as fire safety requirements become stricter worldwide. As a non-combustible material, it is increasingly used in high-risk facilities such as hospitals, schools, and chemical plants. Although heavier and slightly less insulating than PU, mineral wool panels are now the preferred option where fire compliance is non-negotiable.

In response to this shift, companies like Fineagles have adapted their production lines to support mineral wool panel manufacturing, aligning with the industry’s growing focus on safety and compliance.

EPS Sandwich Panels

Expanded polystyrene (EPS) remains a popular choice in developing markets where affordability and basic insulation are key priorities. EPS panels are lightweight, easy to produce, and suitable for housing, warehouses, and general-purpose buildings.

Fineagles’ EPS production lines allow manufacturers to enter cost-sensitive markets while maintaining consistent panel quality.

Steel vs Aluminum in Outer Skins

Steel Remains the Preferred Choice

When it comes to outer materials, steel dominates the sandwich panel manufacturing market because it offers:

- High strength and durability

- Excellent fire resistance

- Lower cost compared to aluminum

- Compatibility with industrial and non-residential applications

It is widely used in industrial and non-residential construction, making it the standard for large-scale projects.

Aluminum Growing in Niche Applications

Aluminum is steadily expanding into niche applications where corrosion resistance, design flexibility, and aesthetics matter most, such as airports, retail projects, and coastal environments.

Regional Breakdown of the Manufacturing Market

Asia Pacific Leads Global Production and Demand

In 2023, Asia Pacific held 47.93% of the global sandwich panel manufacturing market, the largest share by region. Key contributors include:

- China: Rapid industrialization and massive infrastructure projects

- India: Smart Cities Mission, affordable housing, and cold chain expansion

- Southeast Asia: Rising construction activity in Indonesia, Thailand, and Vietnam

To meet rising domestic and export demand, local manufacturers are scaling up production lines.

North America: Innovation and Sustainability Focus

The U.S. and Canada are experiencing steady demand for insulated metal panels, particularly in warehousing, data centers, and modular buildings. The region’s sandwich panel market is projected to reach USD 3.35 billion by 2032, supported by incentives for energy-efficient construction and investments in sustainable materials such as low-GWP foaming agents and recycled steel.

Europe: Strict Fire Safety and Sustainability Codes

Europe represents one of the most regulated sandwich panel markets, with strict fire safety and environmental standards. Countries like Germany, France, and the UK are driving retrofitting initiatives, replacing outdated building materials with insulated sandwich panels to improve energy efficiency.

Challenges Facing the Sandwich Panel Manufacturing Industry

Fire Performance Concerns

High-profile building fires have led to bans or restrictions in places like the UAE and parts of Europe, because some foam-core panels have low fire resistance.

Although fire-retardant treatments exist, they increase cost and weight. This undermines the lightweight advantage that makes sandwich panels attractive in the first place.

Market Fragmentation and Limited Innovation

The sandwich panel manufacturing market is highly fragmented, with many regional players offering similar products, leading to intense competition and slow innovation.

Even though companies like Tata Steel, Assan Panel, and DANA Group are investing in R&D, true breakthroughs, such as bio-based cores or self-inspecting smart panels, remain limited.

Future Outlook for Sandwich Panel Manufacturing

Looking ahead, three trends will define the next phase of growth:

- Sustainable Materials: Because of rising environmental demands, there will be increased use of recycled steel, bio-polyols, and low-carbon production methods.

- Smart Integration: As buildings become smarter, panels will be embedded with sensors for temperature, humidity, and structural monitoring.

- Customization via Digital Production: Because project-specific designs are in demand, on-demand panel sizing and finishing will be enabled through automated manufacturing lines.

Manufacturers adopting automation, sustainability, and safety standards will lead the market forward. Companies like Fineagles, with their automated production lines designed to reduce material waste and energy use, reflect how the industry is moving toward greener, more efficient manufacturing.

Sandwich Panel Manufacturing on the Rise

The sandwich panel manufacturing market size is set for strong expansion, reaching USD 20.51 billion by 2032. Driven by urbanization, cold chain growth, and the global push for energy-efficient buildings, this sector is more than just a construction trend—it’s a structural shift in how we build.

As manufacturers adapt to stricter fire codes, environmental regulations, and customer demands for faster, smarter solutions, innovation will become the key differentiator.

For businesses in construction, logistics, or industrial development, now is the time to understand and leverage the power of advanced sandwich panel systems.

Frequently Asked Questions

What is the market size of the global sandwich panel?

The global sandwich panel market reached USD 9.91 billion in 2023 and is anticipated to grow to USD 20.51 billion by 2032 at a compound annual growth rate (CAGR) of 8.4% during the forecast period.

What’s propelling the growth of the sandwich panel market?

Growing demand from industrial buildings, commercial buildings, and cold storage, and government initiatives to improve storage facilities are driving growth. Industrialization, rapid urbanization, and the need for energy-saving and fast-installation construction materials are also propelling the market forward.

What’s the forecasted CAGR of the market between 2024 and 2032?

The market will expand at a CAGR of 8.4% from 2024–2032.

Which region holds the majority of the global sandwich panel market at present?

The Asia Pacific region led the market in 2023 with a 47.93% share because of increasing demand in countries like China, India, and Southeast Asia.

What are the major uses of sandwich panels?

Sandwich panels find extensive applications in non-residential buildings like cold storage warehouses, industrial structures, and commercial buildings. Due to their thermal insulation and low weight, the panels are also found suitable for domestic construction.

What are the latest trends affecting the sandwich panel industry?

Major trends include a growing focus on sustainable construction, more demand for energy-efficient insulation materials, and extensive use of modular building systems. Environmentally friendly and fire-resistant panel designs are also being innovated by manufacturers.

What materials do sandwich panels most often incorporate?

The highest used core materials include polyurethane, polystyrene, and mineral wool. Steel is the most used for exterior layers due to its fire-resistance and affordability, while aluminum is used more for its adaptability and light structures.

What are some challenges facing the sandwich panel market?

One of the main problems is the low fire resistance of some lightweight foam-core panels. Though they offer excellent insulation, they may not meet fire safety standards. Fire-resistant versions are generally heavier and more expensive, thereby limiting some of their applications.

What are the major companies in this sector?

Key players include Kingspan Group (Ireland), Tata Steel (India), Sintex Group (India), ArcelorMittal (Europe), and Assan Panel A.S. (Turkey). These companies are focusing on strategic acquisitions, product innovation, and regional expansion to strengthen their market position.

Get Ahead in the Market

Looking to expand your role in the global sandwich panel industry? Fineagles Advance Engineering provides customised solutions from PU/PIR and mineral wool continuous lines to EPS and flexible facing systems, all backed by 24/7 support and expert training.

Request your free feasibility study or factory layout consultation today and discover how Fineagles can help you scale production with confidence.